Will cognitive biases will kill AI strategy?

The threat to capex, returns, and risk management of AI

The TL;DR

AI does not make leaders irrational. It gives their irrationality a larger budget, and a faster clock.

The most expensive AI failures of the next three years will not come from poor technical choices. They will come from a single decision error: leaders relying on the inside view — what we plan to do, what our team is capable of, what our timeline assumes — when the outside view would tell them, in five minutes, that 80% of comparable projects fail.

Daniel Kahneman called this the most consequential bias in human judgement. Bent Flyvbjerg has spent thirty years documenting its cost across 16,000 major projects. The fix has a name — reference class forecasting. The 2023–2026 AI cohort gives us, for the first time, a reference class that boards can actually use.

Most are not using it.

What follows is an examination of four boardroom biases that AI has industrialised. They are the usual suspects: sunk cost, planning fallacy, overconfidence, status quo. But the unifying lesson is not that boards need to memorise more biases. It is that they need to stop reasoning from the inside.

Part I: Biases that add risk and kill ROI

What follows is a 2026 rework of a 2015 article: Boardroom Biases Kill Strategy. The exam question - what lessons does the past teach? Which learnings no longer apply?

The fish rots from the head

In 1996, FoxMeyer was the fourth-largest pharmaceutical distributor in the U.S., a $5 billion company. They bet their future on a massive ERP (Enterprise Resource Planning) transformation—an SAP implementation designed to revolutionize their supply chain. It was supposed to be the “technological edge” that would crush their competition.

Instead, it crushed them. Within a year of the “go-live,” FoxMeyer filed for bankruptcy and was sold off for pennies on the dollar.

Humans make mistakes and enterprises fail, but some of those mistakes are systematic errors, that is, non-random and directionally “biased.” (Projects never undershoot on time, cost, and quality by a factor of two; they sure do overshoot, though.)

Understanding and managing boardroom biases, your own, dear leader, and your team’s, is an essential and undiscussed leadership skill.

Before we start, if you immediately thought of ten reasons why the FoxMeyer example won’t happen to you, that is the Optimism Bias and Probability Neglect at work—tricking you into rounding a real risk down to zero.

Potted history of cognitive biases in boards

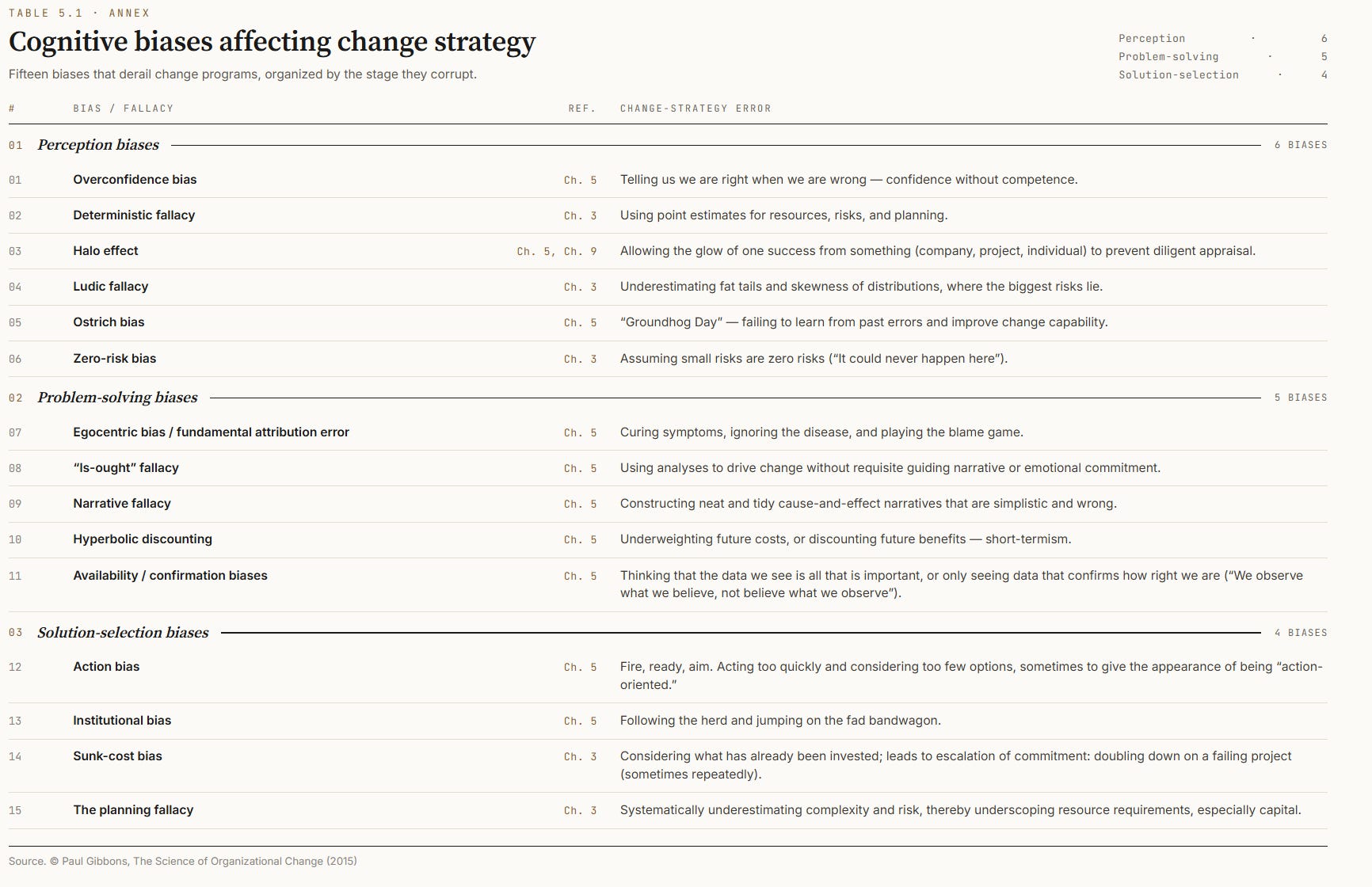

Starting in the 1950s, thinkers like Herbert Simon began to wonder how humans really made decisions and why they deviated from rationality so much. Soon after, Kahneman and Tversky began their partnership that resulted in a Nobel - again, the question they turned their mind to was “what are we systematically and predictably doing wrong?” By the time the 21st century was rolling, we had this:

Don’t worry that you can’t read it; it is substantially accurate and completely useless. What are leaders supposed to do? Memorize all hundred of them?

When I started writing The Science of Organizational Change, that was the state of play — a long list of impossible-to-use biases and fallacies. But I was running a leadership consulting firm and felt this OUGHT to be useful if we could distill it down and provide guidance on what leaders should do about a far smaller number.

What follows are the four biases that, in my experience, do the most damage in boardrooms when making technology investment decisions. Part II will cover the social and group biases — groupthink, authority bias, the halo effect — the ones that corrupt how boards interact. This piece is about the ones that corrupt how boards think.

The “rational” boardroom myth

The core message was that directors are not rational actors; they are, as Dan Ariely put it, “predictably irrational.” That message landed with some discomfort and a lot of nodding.

Today, the stakes are considerably higher. Boards are approving AI capital expenditure at unprecedented speed, often with less technical understanding than they had during the ERP era. We assume billion-dollar decisions are made with spreadsheets and logic. In reality, they are driven by what Keynes called “animal spirits” — confidence, fear, herd behavior, and the intoxicating narrative that this time, the technology really will deliver on the pitch deck.

The cost of getting this wrong is not abstract. McKinsey’s research found that 17% of large IT projects go so badly they threaten the very existence of the company. Not “underperform.” Not “come in over budget.” Threaten the existence of the company. When you sit in a boardroom approving a nine-figure AI transformation, that number should be written on the wall.

Bias #1: The sunk cost fallacy

The sunk cost fallacy — sometimes called escalation of commitment — is the tendency to justify increased investment in a failing endeavour based on what has already been spent. “We’ve come this far” is the sentence that destroys shareholder value.

The textbook case is Nick Leeson and Barings Bank. Leeson doubled down on losing derivative positions to hide earlier losses, eventually accumulating $1.3 billion in exposure that brought down the oldest merchant bank in Britain. The psychology that drove Leeson is the same psychology that drives every executive who refuses to pull the plug on a failing implementation.

I used to explain this to boards with the theater ticket analogy. You paid $180 for a play. A blizzard hits. You’re ill. The reviews are terrible. Do you go? Most people say yes — because they paid $180. But the $180 is gone whether you go or not. The rational question is: “Will I enjoy the next three hours more at the theater or at home?” The money is irrelevant. It is sunk.

Now apply that to AI. A company buys expensive enterprise AI licenses — say, Copilot at scale — or sinks eighteen months into building a custom LLM. Six months in, adoption is low, the use cases haven’t materialized, and the data quality problems are worse than anyone admitted. The rational response is to pivot or cut. The human response is to double the budget, hire consultants, and launch a “change management initiative” to fix the adoption problem. Because we’ve already spent the budget.

The worst part is sunk cost reasoning can be thought of as virtuous: “When the going get tough, the tough get going.”

That is sometimes an indication of good character - but not without a rational evaluation that starts with - is the cost-benefit analysis from here rational. The most storied example from business is Andy Grove and XX Moore thinking about Intel’s memory business - they asked themselves, so the legend goes, “if we parachuted into this company with no history or emotional attachment to being ‘the memory company,’ what would we do? We would get out. And so they did. (If they had a crystal ball that could peer into 2026, they might have concluded differently!)

The antidote is simple in theory and brutal in practice: make it psychologically safe to kill projects and admit we were wrong.. If every cancelled initiative is treated as a failure of the person who championed it, no one will ever cancel anything. The sunk cost fallacy doesn’t survive in cultures where pivoting is rewarded, but it thrives in cultures where admitting a mistake is career-ending.

Bias #2: The planning fallacy

The planning fallacy is the systematic tendency for project plans to undershoot actual costs and timelines. Not by a little. Not occasionally. Systematically, and by a lot.

The research here is unambiguous. Large IT projects run an average of 45% over budget and deliver 56% less value than predicted. That isn’t bad luck. That’s a structural feature of how humans estimate complex undertakings. We anchor on the best-case scenario and treat it as the most likely scenario. We plan for the world where nothing goes wrong, then act surprised when things go wrong.

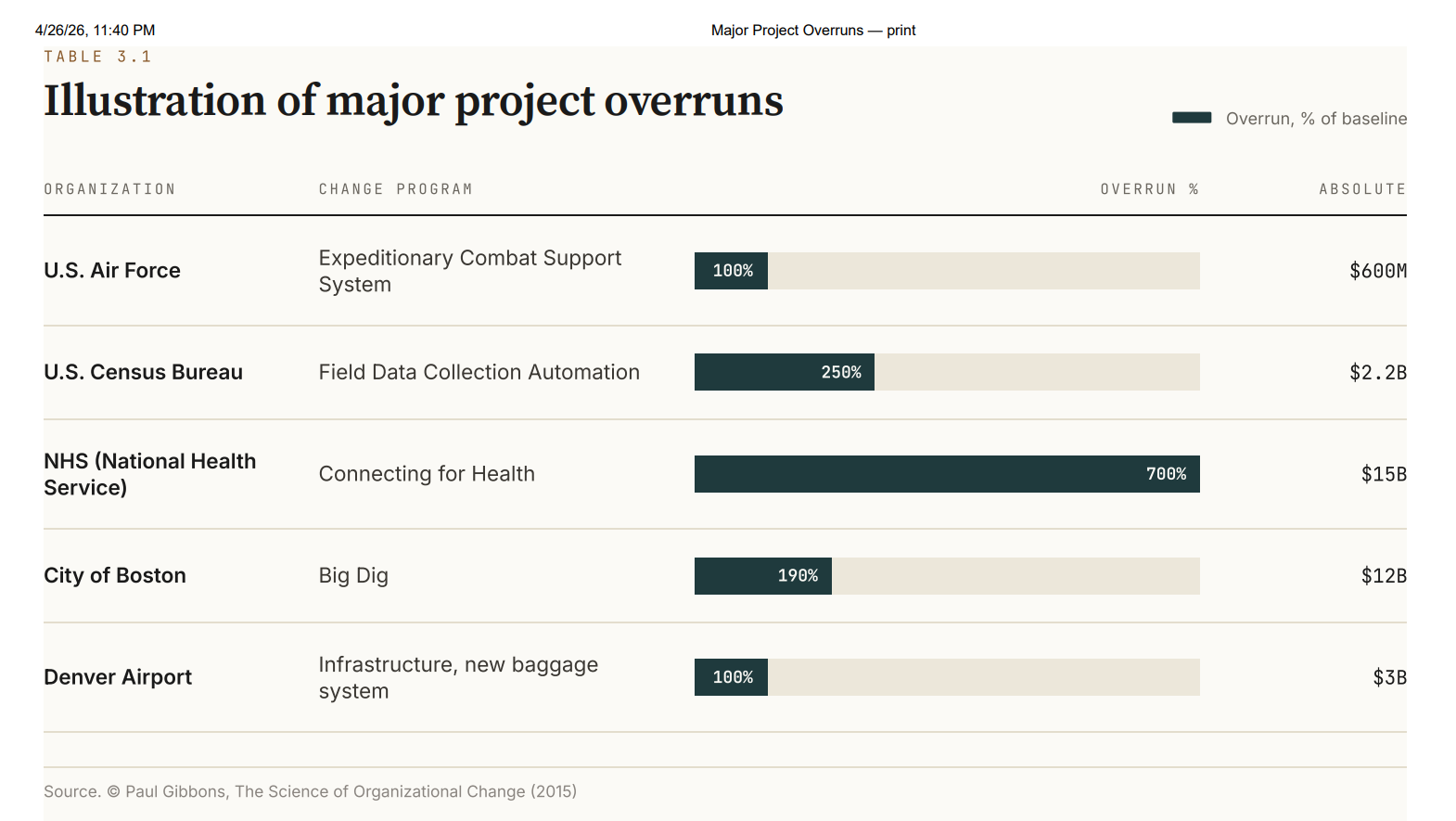

The canonical example is Denver International Airport’s automated baggage system. It was supposed to revolutionize airport logistics. It ended up $3 billion over budget, years late, and was eventually ripped out entirely. The engineers weren’t incompetent. The technology wasn’t impossible. The planning was delusional — and nobody in the approval chain had the incentive or the courage to say so.

The AI version of this is boards approving AI integrations as though they are “plug and play.”

The pitch deck shows the model; it doesn’t show the iceberg underneath — the data cleaning, the governance framework, the change management, the retraining, the integration with legacy systems, the edge cases that only surface at scale. A board that approves an AI transformation without explicitly budgeting for the iceberg is not making a brave bet. It is making a planning fallacy with other people’s money.

Bias #3: Overconfidence

Overconfidence — hubris, if you prefer the Greek — is the gap between confidence and competence. It is the most dangerous bias in a boardroom because it is the one most correlated with seniority. The higher you rise, the more your confidence is reinforced and the less your competence is tested.

Dick Smith Electronics, the Australian retailer, is a case study. The board believed they could move massive inventory volumes despite clear market signals that consumer electronics retail was contracting. They weren’t stupid. They were overconfident — and overconfidence made the disconfirming evidence invisible.

In AI, overconfidence takes a specific and measurable form.

About a quarter of Fortune 500 companies now have a Chief AI Officer — up from one in ten two years ago. But Heidrick & Struggles finds that nearly half of those titles are simply reclassified existing roles — the CIO or CTO with new business cards. Strip those out, and only about one in eight Fortune 500 companies has a dedicated, net-new AI leader. That's the answer to the question of whether the C-suite has caught up. It hasn't.

This is not a skills gap. It is a structural vulnerability. A board that cannot interrogate an AI strategy is a board that will approve whatever the most persuasive presenter recommends.

And the definition matters. 'AI expertise' on a skills matrix can mean anything from 'sat on a generative AI panel at Davos' to 'ran a $200m ML platform.' If you set the bar at the latter — operating experience that lets you ask the second and third question, not just the first — the number collapses. The Conference Board's S&P 500 data puts disclosed AI expertise at 2.7% of directors. Deloitte's global survey finds two-thirds of directors say their boards have 'limited to no knowledge or experience' with AI. The figures most often quoted in the 10–15% range sit between these, and depend almost entirely on whether the researcher counted self-disclosure or independently verified track record. Whichever number you choose, the conclusion is the same: the overwhelming majority of boards approving AI strategies cannot distinguish a credible plan from a slick deck.

The corrective is not “get smarter about AI” — that’s a years-long journey. The corrective is epistemic humility: know what you don’t know, and build decision processes that compensate. Pre-mortems, red teams, independent technical review, and the discipline to ask “what would have to be true for this to fail?” before asking “how do we make this succeed?”

Bias #4: Status quo bias

Status quo bias is the preference for things to remain as they are. It is not laziness. It is a deep psychological preference for the known over the unknown, reinforced by loss aversion — the well-documented finding that humans feel losses roughly twice as intensely as equivalent gains.

Kodak invented the digital camera. They held the patents. They had the engineering talent. And they chose not to cannibalise their film profits, because the film business was profitable now and digital was uncertain later. By the time “later” arrived, it was too late. Kodak filed for bankruptcy in 2012.

The AI version of this is playing out in boardrooms right now. The idea that having been successful for 25 years gives you a leg up today is a cognitive mistake I hear over and over. Past results are weak predictors of future success. In fact, the world owes Clayton Christiansen a debt - because he raised the counter-intuitive idea that past success might be a trap.

This happens structurally - the company “stack” (structures, systems, mindset) is perfectly synced with a world that no longer exists.

In the “intelligence transition” — a fundamental shift in how knowledge work is produced, evaluated, and valued. The last time something comparable happened was the internet, and the companies that treated the internet as “just a new channel” are mostly gone.

Status quo bias is particularly insidious because it doesn’t feel like a decision. Not acting feels like not deciding. But in a rapidly shifting environment, not acting is a decision — it is a decision to let competitors, market shifts, and technological change determine your future for you.

The solution: the outside view

So what do you do? You cannot eliminate these biases — they are features of human cognition, not bugs in your particular board. But you can build processes that compensate.

The most powerful tool I know is Reference Class Forecasting. The logic is elegant: instead of asking “how long will our project take?” — which invites every bias on this list — you ask “how long did similar projects take?”

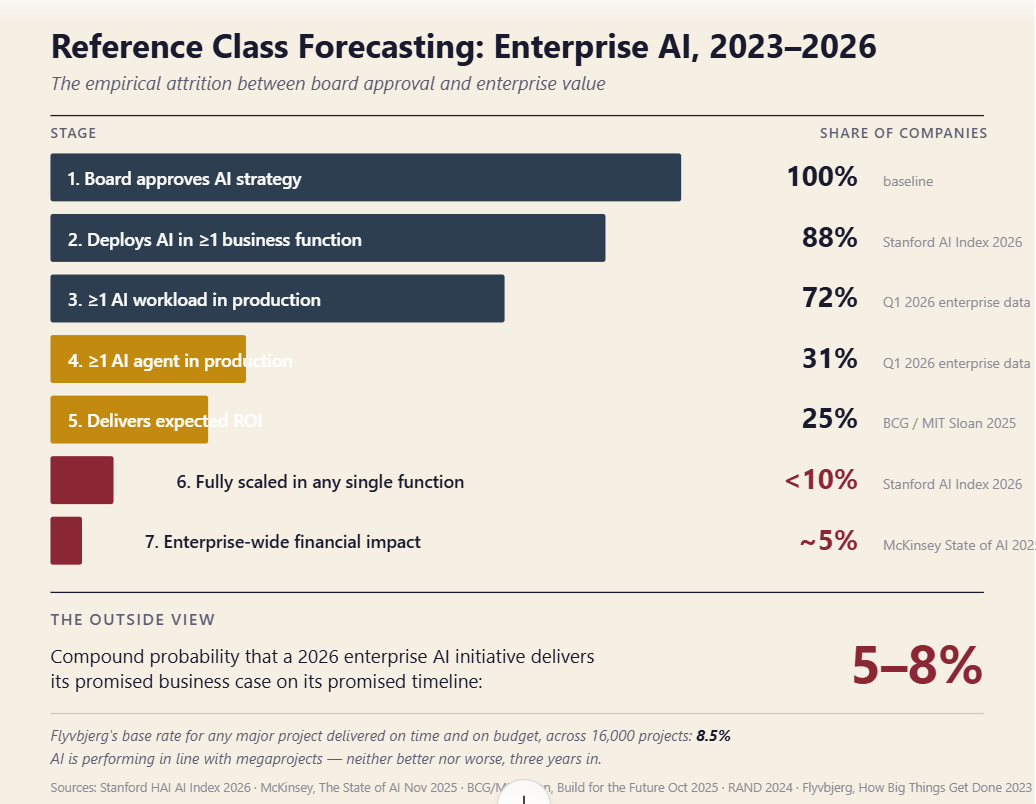

If you buy Flyvbjerg’s well researched conclusions, 8.5% of IT projects come on on time and on budget. That is pre-AI research - but ask yourself, “is this easier or harder?”

Three years into the gen AI cycle, the answer is bracing. RAND finds that 80% of AI projects fail — twice the rate of non-AI IT projects. McKinsey finds that only 5.5% of organizations are seeing real financial returns at the enterprise level. BCG finds that the median company has been at this for 24 to 30 months and shows no meaningful EBIT impact. That figure — 5.5% — is within rounding distance of Bent Flyvbjerg's 8.5% base rate for any major project coming in on time and on budget, drawn from his 16,000-project database.

In other words: the AI cohort is so far behaving exactly like every other major project class in history. Worse, on some measures. The inside view says this time is different. The outside view says it isn't.

The hard news: fewer than 10% have fully scaled AI in any single business function. That second number has not meaningfully moved in three years — not when GPT-4 launched, not when reasoning models arrived, not when agents went mainstream. The technology has improved on every dimension we can measure. The organizational ability to deploy it at scale has improved on almost none. Reference class forecasting tells us the binding constraint is not the model. It is the board, the C-suite, and the change capability beneath them.

That question forces you out of the “inside view” (your narrative, your optimism, your special circumstances) and into the “outside view” (the base rate for projects like yours). In a study of Hong Kong road projects, Reference Class Forecasting determined that a 44% budget uplift was necessary to reach 80% certainty of completion within budget. Forty-four percent. That is the gap between how humans plan and how projects actually unfold.

Combined with pre-mortems — “assume this project has failed; write the post-mortem now” — Reference Class Forecasting gives boards a fighting chance against the biases described above. It doesn’t make you rational. It makes you less predictably irrational, which in a world of nine-figure AI bets is worth quite a lot.

What’s next

We cannot eliminate biases, but we can build processes to mitigate them. This piece covered the four that corrupt how boards think — sunk costs, planning fallacy, overconfidence, and status quo bias.

Part II covers the ones that corrupt how boards interact: Groupthink, Authority Bias, and the Halo Effect. These are the “culture killers” — the social dynamics that cause smart people in a room together to agree on terrible ideas, defer to the loudest voice, and mistake charisma for competence.

Part II: The “Culture Killers” (Social & Group Biases) is coming next.

A focus on how the board interacts—Groupthink, Authority Bias, and the Halo Effect. This is about people and governance.

Further reading:

“Biases in the Boardroom” — Gibbons, P. (2016). Presentation to University of Denver Daniels School of Business faculty

Keynes, J.M. (1936). The General Theory of Employment, Interest and Money. “Animal spirits” as the driver of economic decisions beyond rational calculation.

Bloch, M., Blumberg, S., & Laartz, J. (2012). “Delivering Large-Scale IT Projects on Time, on Budget, and on Value.” McKinsey Digital.

Staw, B. (1976). “Knee-deep in the Big Muddy: A Study of Escalating Commitment to a Chosen Course of Action.” Organizational Behavior and Human Performance.

Leeson, N. (1996). Rogue Trader. The Barings Bank collapse — $1.3 billion in losses from escalating derivative positions.

Gibbons, P. (2015). The Science of Organizational Change. Theater ticket analogy for sunk cost reasoning.

Kahneman, D. & Tversky, A. (1979). “Intuitive Prediction: Biases and Corrective Procedures.” TIMS Studies in Management Science.

Flyvbjerg, B. & Budzier, A. (2011). “Why Your IT Project May Be Riskier Than You Think.” Harvard Business Review.

de Neufville, R. (1994). “The Baggage System at Denver: Prospects and Lessons.” Journal of Air Transport Management.

ASIC v Dick Smith Holdings (2018). Australian Securities and Investments Commission findings on inventory management failures.

Cheatham, B., Javanmardian, K., & Samandari, H. (2019). “Confronting the Risks of Artificial Intelligence.” McKinsey Quarterly.

Lucas, H. & Goh, J. (2009). “Disruptive Technology: How Kodak Missed the Digital Photography Revolution.” Journal of Strategic Information Systems.

Gibbons, P. (2026). “Intelligence transition” — the framing that AI represents a shift in cognitive infrastructure, not a software deployment.

Flyvbjerg, B. (2006). “From Nobel Prize to Project Management: Getting Risks Right.” Project Management Journal.